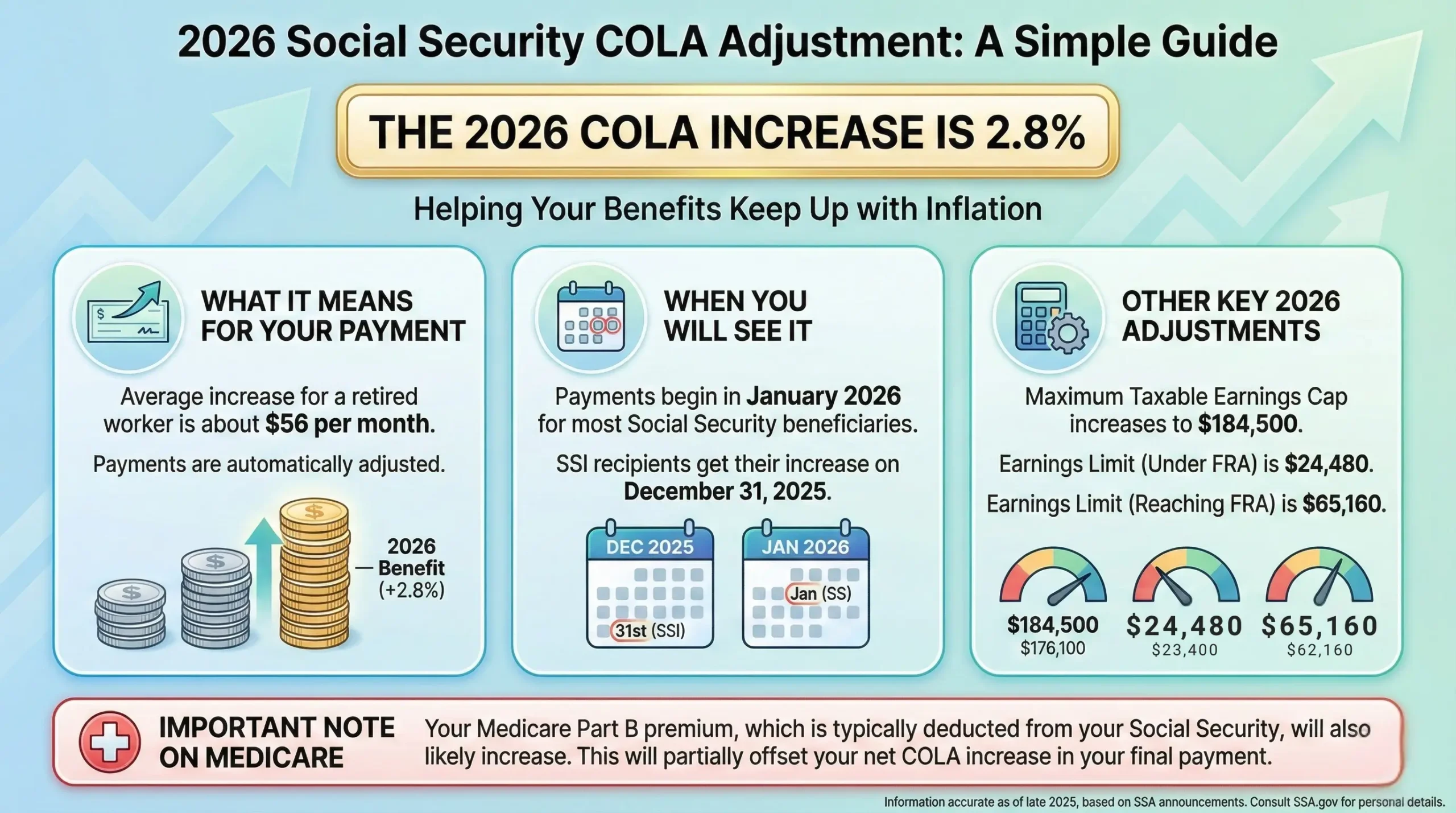

Social Security benefits are getting a 2.8% cost-of-living adjustment (COLA) for 2026. That sounds straightforward: your monthly benefit goes up to help keep up with inflation. But many retirees notice something frustrating in January—your bank deposit may rise by less than 2.8% (or less than you expected).

The reason is simple: COLA increases your gross benefit, but your net check is your gross benefit minus deductions like Medicare premiums, taxes/withholding, and other items that can change year to year.

What is the Social Security COLA?

The COLA is an automatic yearly increase that helps Social Security benefits keep pace with inflation. Social Security calculates it using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), comparing last year’s third-quarter average to this year’s third-quarter average.

What does a 2.8% COLA look like in real dollars?

A 2.8% COLA means your monthly benefit is multiplied by 1.028. Here are a few quick examples (gross amounts, before deductions):

$1,200/month becomes about $1,233.60 (about +$33.60)

$1,500/month becomes about $1,542.00 (about +$42.00)

$2,000/month becomes about $2,056.00 (about +$56.00)

Social Security has estimated the average retired worker benefit increases by about $56/month with the 2026 COLA. Your personal increase may be higher or lower depending on your benefit amount.

COLA vs. your bank deposit: use the quick calculator

COLA 2026 Net-Check Estimator 2.8% default

This estimates how your net deposit can change after typical deductions (especially Medicare Part B).

Enter what applies to you—leave anything you don’t have as $0.

Use your gross benefit amount (before Medicare premiums, taxes, etc.).

Set to 2.8 for the 2026 COLA, or change it for “what-if” planning.

If you pay Part B directly (not from your Social Security check), put $0.

Standard premium is shown by default. If you pay IRMAA, enter your total Part B amount.

Examples: Medicare Advantage premium, union dues, garnishments, or other withholdings.

If nothing changes, keep it the same as above.

If you don’t withhold taxes from Social Security, choose “None”.

If “Percent,” enter a number like 7 (for 7%). If “Dollar,” enter the monthly amount.

New gross benefit (after COLA)

$0.00

Estimated net deposit now

$0.00

Estimated net deposit in 2026

$0.00

Estimated change in your net deposit

$0.00

How much of your COLA increase is “used up” by higher deductions

$0.00

Note: This is a planning estimate. Your actual deposit may differ due to SSA rounding, Medicare billing timing,

income-related premiums (IRMAA), state taxes (in some cases), and other individualized deductions.

Why your net check might not rise much in January

COLA raises your Social Security benefit, but deductions can rise too. Here are the most common reasons your net deposit grows by less than your COLA:

1) Medicare Part B premiums often rise—and many people have them deducted from Social Security

For 2026, the standard Medicare Part B premium is $202.90/month, up from $185.00 in 2025. If your Part B premium comes out of your Social Security benefit, that increase can offset part of your COLA.

Example: if your gross benefit rises about $56/month, but your Part B premium rises $17.90/month, your net gain could be closer to about $38/month before any other changes.

2) Income-related Medicare premiums (IRMAA) can reduce (or erase) your COLA for higher earners

If your income is above certain thresholds, Medicare adds an income-related monthly adjustment amount (IRMAA) to Part B (and Part D). If you move into a higher bracket—or if your premium changes—your net Social Security deposit can rise only slightly (or even fall).

3) Your tax withholding can change what hits your bank account

Some people choose to have federal income taxes withheld from Social Security. If you withhold a percent of your benefit, the withholding generally rises as your benefit rises. That means a portion of the COLA may be diverted to taxes automatically.

4) Other deductions can change year to year

Medicare Advantage plan premiums (if deducted from Social Security)

Optional withholdings (like union dues or voluntary repayments)

Garnishments or court-ordered deductions (if applicable)

Overpayment recovery arrangements (if applicable)

5) The “hold harmless” rule can also affect what happens

In some cases, Medicare rules can limit how much your Part B premium increases if the premium hike would otherwise reduce your Social Security payment. This doesn’t apply to everyone (for example, it generally does not protect people who pay IRMAA or those who are billed for Part B premiums instead of having them deducted from their Social Security).

What you can do now (simple checklist)

Compare gross vs. net: Look at your gross benefit, then list deductions (Part B, other premiums, taxes).

Watch Medicare premium changes: If you pay more than the standard Part B premium, confirm whether IRMAA applies.

Re-check withholding: If you withhold taxes as a percentage, expect the withheld amount to rise with COLA.

Plan January budgeting realistically: Use the calculator above to estimate your “new normal” net deposit.

Keep an eye out for SSA notices: Your COLA-adjusted benefit notice (and Medicare premium changes) help explain any net difference.

Quick FAQ

When will I see the 2.8% increase?

The 2.8% COLA is reflected in Social Security payments issued in January 2026 (for most recipients).

Does COLA apply to SSI too?

Yes, SSI federal payment amounts also increase with the COLA (though your actual payment depends on your situation and any state supplements).

Why did my friend’s check go up more (or less) than mine?

Even with the same COLA, net results vary based on Medicare premiums, IRMAA, tax withholding, and other deductions. Two people can have the same COLA percentage and still see different net deposits.

Browse thousands of Senior Centers from around America. Senior Centers are an integral part of society and are the center of life for many seniors and aging adults.

Find a Senior Center which fits your needs using our search feature and keep up to date on all the latest news.

Advertisers are not endorsed by SeniorCenters.com or any senior center listed. This site is not endorsed by or affiliated with any senior center or organization listed.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behaviour or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.